Nathan's Famous: Framing an investment in Sept. 2020

Nathan's Famous: Framing an investment in Sept. 2020

Diligence Report | 30 min read | How I framed this opportunity as a buy-and-hold investor

Originally published on midstoryventures.com in September 2020.

Before you read this segment in the Diligence Report series — please read the “Introduction: Diligence Report Series” post here.

Navigation:

More Than a Restaurant

A Unique Business Model

Nathan’s Famous is more than a restaurant. As a company who has built their business on hotdogs, Nathan’s has one of the most unique models in the industry.

Nathan’s Famous was started in 1916 as a small hotdog stand in Coney Island. Over the most recent decades, the company has transformed its business model.

Most restaurants ask the question, “how do we get customers to come to our store?”

Nathan flips this model on its head. The company asks the question, “how do we get our food in front of our customers?”

This “north star” has led to Nathan’s building a one-of-a-kind business model.

The company has three business lines: Restaurant Operations, Licensing, and Branded Products Program. Its company-owned and franchised restaurants deliver the Nathan's experience through its store. Its Licensing business delivers the Nathan’s experience through supermarkets across the country. Its Branded Products Program delivers the Nathan’s experience through its restaurant, movie theater, convenience store, and sports stadium partners.

While some restaurants have been able to franchise their concept, and some others have even been able to license their products, Nathan’s is the only company who has been able to franchise, license, and sell their concept to other restaurants and sports stadiums.

A High-Quality Business

Nathan’s does approximately $100M in revenue every year. The investment requirement is in its Restaurant Operations business; the rest are capital-light. Of the 220 restaurants it has, Nathan’s only owns 4 of them. This results in a high cash flow business.

As you can imagine, a business model like this can generate extremely high operating margins, free cash flow conversion, and returns on invested capital.

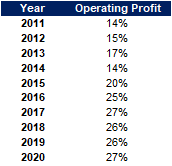

Nathan’s operating margin is 27%, and it has been increasing every year. This is extremely high, even compared to franchised-focused restaurant systems like Wingstop. Wingstop has margins of 25%.

Nathan’s margins even trump the largest restaurants in the world: Chipotle (16%), Starbucks (16%), and Domino’s (13%). As Nathan’s margin grows, it will earn its place among the best of the best: McDonalds (30%) and Restaurant Brands (38%).

Only the best-in-class restaurants can obtain a free cash flow conversion of 100%. Nathan’s free cash flow conversion is even better than the best-in-class restaurants.

The company’s free cash flow margin is greater than 100% every year in 8 out of the last 10 years. And in 2 of those 8 years, the company’s free cash flow margin was more than 300%.

As Nathan’s Licensing business became a larger and larger percentage of the business, the company’s returns on invested capital grew higher and higher. By 2016, the company had achieved returns on capital greater than 100%.

This trend is expected to continue as long as the company keeps its capital expenditures to a minimum.

The Nathan’s Famous Experience

Nathan’s brand, more specifically the Nathan’s experience, is the reason for the company’s high-quality business model.

Coney Island, the home of Nathan’s Famous, has been a seaside resort and amusement park since 1895. Between about 1880 and World War II, Coney Island was the largest amusement area in the United States, attracting several million visitors per year.

At the time, Coney Island was so crowded on summer weekends that New York City parks commissioner Robert Moses observed that “a coffin would provide more space per person than the beach.”

The following pictures give you an idea of how popular Coney Island was.

Nathan’s Famous was very much part of the magical Coney Island experience. In fact, some say that Nathan’s Famous is synonymous with New York — a true symbol for the city.

In those days, the most convenient way to get to Coney Island was by train. Once you got off the train and made it through the passageway, you would see the original Nathan’s Famous hotdog stand. This location was so important to the success of the business that when NYC extended the subway to Coney Island (four subway lines now), business immediately boomed. On any given weekend, Nathan’s was serving around 75,000 hot dogs.

At the time, Nathan’s offered their hotdogs for 5 cents, half of what everyone else charged on the island. They quickly became known for delivering “quality food at a fair price.”

For many New Yorkers and out-of-country visitors, Coney Island represented a nostalgic time: eating Nathan’s Famous hotdogs while hearing the rumbling of rollercoasters and smelling the salty ocean in Coney Island. These were fond memories when talking to different people during my research.

At one point, Nathan’s popularity even started to expand to resonate with celebrities.

Nelson Rockefeller (41st Vice President and son of John D. Rockefeller) once said, “No man can hope to be elected in his state without being photographed eating a hot dog at Nathan’s Famous.” Jacqueline Kennedy (wife of President John F. Kennedy) loved Nathan’s hot dogs so much that she served them at The White House.

The people of this generation told their children the story about Coney Island and even took them to experience it themselves. Their children would tell their children, and so on. This trend continued until Coney Island became the historic landmark that it is today.

Nathan’s Famous is a brand of nostalgia, convenience, quality, and price.

The foundation of Nathan’s brand is nostalgia — nostalgia of the magical Coney Island experience. It’s nostalgia about New York. A bite into a Nathan’s hotdog transports you to a different time and gives you those memories and feelings. This nostalgia is a big part of the Nathan’s Famous experience.

The nostalgia is the reason why Nathan’s became the largest selling brand (more than $1 million) in the New York supermarkets by the mid-1990s. It is the reason why Nathan’s was named “Official hotdog of the MLB” in 2017. It is the reason why Nathan’s hotdogs are served in restaurants like Auntie Anne’s and Hot Dog on a Stick.

A Closer Look

Strategic Shift

Nathan’s Famous wasn’t always a high-quality business.

In 2000, the company did $37M in revenue. Here’s the breakdown of the revenue.

90% from Restaurant Operations (75% company-owned stores + 15% franchising)

5% from Licensing

5% from Branded Products Program

The operating margin for 2000 was 0%. There are a few things we can learn from this.

The Restaurant Operations business was not turning a profit. We know this because the Licensing business and the Branded Products Program business generates an average of 99% profit margin and 15% profit margin, respectively, every year.

Company-owned stores were the main driver of poor profitability. Management had expanded too fast. Restaurant operating expenses as a percentage of revenue hit an all-time high of 22%.

A proper franchising system should generate at least 30% in pre-tax profits. However, Management picked poor locations for its franchises and acquired poor-performing franchises from other brands. The average unit volume (AUV) for each franchise was extremely low. As a result, the high profit margins from the franchising business were not large enough to produce a profit beyond 0%.

Nathan’s became a high-quality business in 2015 by cutting the fat and focusing on high-profit, capital-light businesses.

On the Restaurant Operations side, Management sold off its poor-performing, non-Nathan’s brands (Miami Subs and Kenny Rogers Roasters). It reduced the company-owned units down to 5 and franchised units to 296 and increased franchise royalties from 4.0% to 5.5%.

On the distribution side, it developed a total of 53,000 points of distribution — 39,000 from the Licensing business and 14,000 from the Branded Products Program.

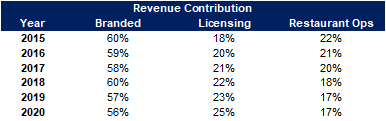

In 2015, the company did $99M in revenue. Here’s the breakdown of that revenue.

60% from Branded Products Program

22% from Restaurant Operations

18% from Licensing

Of the $99M in revenue, 20% was profit. Here’s the breakdown of the profit contribution:

64% from Licensing

20% from Restaurant Operations

16% from Branded Products Program

By doubling down on the brand-marketing and product-distribution strategy, the economics from 2015 to 2020 are much stronger than they were in 2000.

Here’s a breakdown of the revenue and profit contribution with the new model.

Reverse Engineering

Like most of the other companies that I write about, Nathan’s Famous has demonstrated an ability to produce free growth (infinite returns on invested capital). As a result, we do not need to factor in retained earnings for the business to grow.

We can look at the company as an equity bond and then reverse engineer the assumptions baked into the market price.

On any given day, the market offers a 15x EV/FCF (3-year trailing average FCF) for this new and improved business. This represents a 7% free cash flow yield. For a long-term investor looking for an annualized return of 10%, we can reverse engineer the following assumptions.

Nathan’s Famous will never go out of business

Nathan’s Famous will never have a free cash flow margin below 17%

Nathan’s Famous will grow at 3% every year in perpetuity

Nathan’s famous will always have an infinite ROIC

With this framework in mind, we can investigate how likely Nathan’s Famous will be able to pass these hurdles.

How long will Nathan’s Famous last?

The best way to think about Nathan’s durability is by analyzing its longevity and adaptability.

A Predictable Industry

The longevity of the hotdog industry is based on its predictability. This predictability is based on its integration within in American culture.

Ever since 1776, Americans have spent their Fourth of July celebrating the anniversary of independence from Great Britain. And for the past 50 years on Fourth of July, hotdogs have been the main feature of nearly every barbeque.

According to the National Hot Dog and Sausage Council, Americans eat about 150 million hot dogs on Independence Day. During peak “hot dog season,” which is from Memorial Day to Labor Day, Americans consume about 7 billion hot dogs. That’s about 818 hot dogs consumed per second!

Hotdogs are also popular at events other than Independence Day. They’re popular at baseball games, where hotdogs are the #1 ranked food.

Although hotdogs are consumed less than burgers or pizza, they are still an important part of American culture.

Americans eat about 20 billion hotdogs per year, 50 billion burgers per year, and 3 billion pizzas per year (24 billion slices). Hotdogs have a household penetration of 95%.

Brand Durability

The honest truth is that most people don’t can’t tell the difference between a good and bad hotdog.

Some people who are adamant hotdog lovers will say otherwise, but for most people, they wouldn’t be able to describe the difference. That’s why BuzzFeed has videos like Can our contestants spot the $32 hot dog?

It’s also evidenced by the fact that Bar-S, a brand known for its “legitimately terrible” hotdogs, have been the highest selling brand in stores for the past 14 years. They are the cheapest hotdog available. That 14-year record can only mean two things. Either (1) the average Joe doesn’t care about the quality of their hotdogs or (2) the average Joe genuinely can’t tell the difference.

This is why the Nathan’s Famous story and experience is so important.

The durability of the brand starts with Nathan’s Famous restaurants.

The Nathan’s Famous restaurant experience is the only reason why the company has successfully entered distribution points that Wienerschnitzel and other hotdog restaurants cannot.

As we discussed earlier, a large part of that experience, and what makes it special, is the Coney Island experience. In order for people to be “hooked” on Nathan’s, they need to have visited the Coney Island flagship store.

Unfortunately, Coney Island has been on the decline since the glory days in the 1900’s. The Internet is plagued with headlines like New York's faded playground: can Coney Island recapture lost glories? and What’s Left of Coney Island?

Furthermore, COVID-19 has impacted the numbers of searches / visits to Coney Island in 2020. As health risks linger for the next few years, Coney Island and Nathan’s Famous run the risk of becoming less popular.

Recently, the hotdog competition has kept the brand alive.

The company introduced Nathan’s Hotdog Eating Contest back in the 1960’s. The contest brings 40,000+ spectators every year to the event and at a least 1 million more who tune in via ESPN. ESPN has broadcasted the event since 2004 and has signed two consecutive extensions to carry the competition on its networks until 2024.

While the attendance and viewership numbers are impressive, Nathan’s is going to need much more than an eating competition for its brand to have staying power.

As you look into the unit economics of the Restaurant Operations, you can start to see commonly-held concerns about the brand.

The most troubling observation is the decline in units at the company-level and franchise-level. The number of units is an indicator of the brand’s relevancy in different markets.

In the last 5 years, the number of company-units have decayed at a 4% compounded rate and the number of franchise-units at a 6% rate.

It’s clear that the Nathan’s Famous brand exists. We see it in the flagship store economics and the national hotdog eating contest. However, a brand should continuously grow its reach (new customers / new locations), not just its depth (current customers / AUV).

The decline in units highlights the brand’s inability to plant a firm footing outside of Coney Island / New York.

The company’s changes to its menu also raises concerns about the value of the brand.

Think about the companies who have the strongest brands in the food / restaurant industry. Companies like In-N-Out and Wingstop hardly have to change their menu. In fact, the original menu is almost identical to the one that exists today. These are a rare breed.

Most companies change their menu every now and then to keep up with trends and consumer preferences.

However, the menu changes at Nathan’s are different. As Senior Vice President James Walker describes it, it’s a complete “evolution” to the current menu.

On James Walker’s LinkedIn, he describes himself as “a top restaurant industry expert with a specialty in rebranding and repositioning.” On a podcast called Restaurant Executive Mastery, he says he has a knack for “invigorating change.”

James Walker joined Nathan’s Famous in 2019 after spending less than a year and a half trying to save Subway’s North American presence, which was declining by hundreds of units every year.

The essence of the menu change is a pivot away from hotdog restaurant to its new slogan: “The Flavor of New York.”

There are two ways to view the arrival of James Walker and the announcement of the new menu.

The current brand is losing its staying power — Nathan’s Famous hotdogs weren’t enough, hence the need for new products.

The current brand is expanding — Nathan’s Famous hotdogs still offer a strong value proposition. The company is simply expanding the offering to increase its depth and reach.

Change can either be good or bad. It just depends on if change indicates an ability to adapt or an inability to last.

Solvency Risk

Firms with a large amount of debt can be risky.

Since Nathan’s large dividend recap in 2015, its Total Debt/EBITDA has hovered around 5.0x. This is most certainly on the higher end. The majority of investors would agree that a Total Debt/EBITDA under 3x makes sense for the average company.

For a company like Nathan’s that requires virtually no investment, the debt serves as a way to maximize the capital structure and maximize the value of the firm. This is the smart thing to do.

However, there comes a point when debt becomes crippling, especially when a company’s operations are disrupted. COVID-19 is a great example of an unforeseen disruption. While Nathan’s has not released their FY 2021 Q1 financials, it would be safe to assume that Nathan’s, like other restaurants, have been significantly impacted by the pandemic.

The company’s FY 2020 Annual Report discloses “the majority of our franchised locations have been temporarily closed due to their locations in venues that are closed (such as shopping malls and movie theaters) or venues operating at significantly reduced traffic (such as airports and highway travel plazas).” Since COVID-19 only affected their FY 2020 Q4 by two weeks, it is safe to assume that the impacts will be much more significant in Q1 and Q2 of FY 2021.

Shake Shack, a comparable peer to Nathan’s Famous, gives us insight into the impact COVID-19 will have on Nathan’s. Shake Shack’s Q2 of FY 2020 was down by 40% quarter-over-quarter. In the case that Nathan’s Restaurant Operations and Branded Product Program are negatively impacted, the Total Debt/EBITDA might spike to a number closer to 10.

Nathan’s hedges its solvency risk with its cash balance.

The typical company’s operating cash level is 3% of revenue. Nathan’s Famous has about $77M in cash as of FY 2020, which is 75% of revenue. This astronomical cash balance gives the company the ability to absorb any downturn in profits since it has a large debt load.

A better way to evaluate the company’s solvency is Net Debt/EBITDA, where Net Debt is Total Debt less cash. The company’s Net Debt/EBITDA falls around 2.5x, which looks much healthier.

Every investor has different levels of debt they are comfortable with. It’s up to each investor to determine under what circumstances they would be willing to believe that the company has little to no solvency risk.

How profitable can Nathan’s Famous get?

This section will focus on operating profit, rather than free cash flow margin. Operating profit is the first input to free cash flow. The last section will cover the capital expenditures part of the equation.

We’ve already outlined the basics of Nathan’s cornerstones of profitability. To summarize, Licensing is the biggest contributor of profit (about 75%) because the revenue generated from that business is nearly 100% profit. Branded Products contribute about 20% of profit primarily because it is the largest revenue stream, although its margins are slightly higher than Restaurant Operations.

The best way to think about Nathan’s profitability potential is in terms of variable and fixed costs.

Fixed Costs

The company does not have a lot of fixed costs. The main fixed costs are Restaurant Operating Expenses and General & Administration. Management has done an extremely good job at keeping these line items as low as possible.

Restaurant Opex was 10% of revenue in 2005. By 2020, it was only 3% of revenue. Management mainly achieved this by cutting down the number of company-owned units. As a result, company-owned restaurant operating margins rose from 15% to 20%.

General & Administration decreased from 23% of revenue in 2005 to 14% of revenue in 2020. While it grew at a 5% CAGR over the 15 years, the revenue from the high-profit Licensing businesses grew at a faster rate to scale these fixed costs.

By keeping rigorously managing its fixed costs, the company grew its profits at a 15-year CAGR of 20% CAGR, outpacing the 15-year revenue CAGR by 6%.

Variable Costs

In recent years, fixed costs have achieved their maximum economies of scale, so managing variable costs will be the key to future profitability.

The largest variable cost at Nathan’s is Cost of Sales. Cost of Sales is generated from the company-owned Restauration Operations business and the Branded Products Program business.

The following table summarizes the gross margins of Branded Products for the last 10 years.

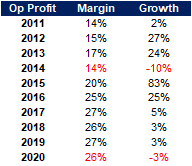

The next table highlights the declines in profitability in the last 10 years.

The two years that the company’s profit took a hit was 2014 and 2020. Notice that those were the same years the gross margins from Branded Products Program took a hit. The Branded Products Program generates at least 60% of the company’s revenue every year, so it contributes a significant portion of the profit.

Now, as we can observe, operating profits don’t necessarily take a hit every time the margin for Branded Products Program decreases. There are a lot more variables to consider than just gross margin for Branded Products.

For example, a decline in the high-profit Licensing business would also be detrimental to profitability. In the last 15 years, the only year that Licensing revenue decreased was 2014. It decreased by 1% due to the one-time transition of suppliers. 2014 was also the same year operating profits decreased by 10%.

The more important takeaway is that a decrease in gross margin can put the company in a vulnerable state. When gross margins take a hit, the company needs to do a lot more to offset the decline in profitability.

How will Nathan’s Famous grow in the future?

Key Drivers

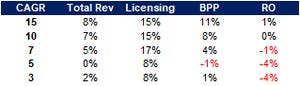

My favorite way to analyze revenue growth is by breaking down the CAGR into several time periods.

It’s a helpful visual to see how growth changes over time. Here’s a breakdown of the revenue growth in the last 15 years.

We can immediately see that Licensing business is the main driver of revenue. When Licensing was growing at double digits, total revenue was growing at mid to high single digits. As it slowed down to 8% in the last 5 years, total revenue growth dropped significantly. Licensing growth has a huge impact on total revenue.

We can also see that Branded Products is a significant revenue driver too. Because it is the largest contributor to revenue, a 2% difference in Branded Products growth (5-year CAGR of -1% to 3-year CAGR of 1%) can mean the difference between flat growth and small growth.

We can expect that these two businesses will continue to be the largest drivers of growth in the future because they represent 80%+ of total revenue.

As a result, the majority of our time should be spent on assessing the growth potential of Licensing and Branded Products Program.

Future of Licensing

Nathan’s has an extremely wide reach in its Licensing business. It has 64,000 points of distribution.

According to the Annual Report, this includes “supermarkets, mass merchandisers and club stores including Kroger, Publix, ShopRite Walmart, Target, Sam’s Club, Costco and BJ’s Wholesale Club located in all 50 states.” This represents nearly all of the grocery stores in the country.

In recent years, the growth in distribution points has slowed. If we expect the number of distribution points to stay at the same level, we can assume that future growth will have to come from volume (within accounts) or price.

Here’s a breakdown of the key licensing metrics of the last 10 years.

Nathan’s Famous has been able to grow its volume despite achieving ~100% penetration across supermarkets in the country. This indicates room for growth within existing accounts through more hotdog sales or different product lines such as crinkle-cut fries and franks-in-a-blanket.

Price is the strongest lever for growth. The company’s ability to increase its overall price in the Licensing business depends on commodity prices, average selling prices (mix of products), and price per unit increases.

The company is highly dependent on its partner, John Morrell, to grow its Licensing business.

In 2015, Nathan’s switched their exclusive hotdog suppliers from SMG to John Morrell. John Morrell has been serving Nathan’s since 2002. Overall, John Morrell has proven to be a valuable partner.

In most industries, companies in a duopolistic industry structure typically exert bargaining power over their customers. The hotdog and sausage manufacturing industry is a duopolistic industry. Smithfield Foods, the parent company of John Morrell, and Tyson Foods are the largest players with 13.0% and 42.5% market share, respectively.

The average profit margin for hotdog and sausage manufacturers is 5.0%. With such a low industry average, Smithfield Foods has an incentive to negotiate a lower royalty rate so they can earn a higher profit.

Instead, John Morrell signed an agreement to pay a 10.8% licensing royalty, 2x higher than the industry average. Prior to 2015, SMG was paying a licensing royalty rate between 3% and 5%. This is a testament to Nathan’s bargaining power. It proves that Nathan’s is a valuable account.

John Morrell is highly incentivized to grow Nathan’s licensing business.

In addition to the 10.8% royalty rate, John Morrell is subject to a minimum annual guaranteed royalties of at least $10 million in the first year of the term (2015). Within the contract, Nathan’s specifies that the minimum guaranteed royalties will increase annually throughout the term.

Since 2015, John Morrell has successfully met the minimum requirement every year.

While this program has worked for the last 6 years, this incentive structure can backfire. Pressures for John Morrell to earn a profit can lead to shortcuts in quality, which has happened with other suppliers in the company’s past, in addition to an overall willingness to compromise Nathan’s desire to achieve the best prices.

In 2017 and 2019, Nathan’s compromised pricing strategy after being persuaded by John Morrell.

Whereas Nathan’s clearly benefits from both pricing growth and volume growth, John Morrell may be more focused with volume growth.

The last part of the exclusive agreement is that John Morrell and Smithfield Foods are required to commit “significant marketing dollars” to the Nathan’s famous brand, both in store and out. Some of the accomplishment since 2015 are listed below:

Nathan’s Famous signs a multi-year partnership to be the “Official hotdog of Major League Baseball”

Nathan’s Famous signs a multi-year partnership to be the “Official hotdog of Six Flags”

Smithfield Foods helps Nathan’s develop and introduce an All Natural hotdog to take advantage of the “clean label” trend

Future of Branded Products

Nathan’s Branded Products Program is built on the success of other venues.

The business has 14,000 distribution points, selling their core products to the following venues:

Sports arenas — New York Yankees, New York Mets, Brooklyn Nets, New York Islanders, Dallas Cowboys, Miami Marlins, Colorado Rockies and Green Bay Packers

Restaurants — Johnny Rockets, Auntie Anne’s, and Hot Dog On A Stick

National movie theaters — Regal Entertainment and National Amusements

Convenience store chains — Race Trac and Holiday Station

Casino hotels — Foxwoods Casino

Airports — through foodservice companies like HMSHost

It is crucial that the customer count grows at these places. Nathan’s Branded Products Program only grows when these venues grow.

Similar to the Licensing business, the growth of distribution points in the Branded Products Program seems to have stalled. Here’s a breakdown of the key licensing metrics of the last 10 years.

In fact, the number of distribution points has decreased from 2012. Naturally, when the company had the most distribution points, it was the only time they achieved double digit volume growth.

Since 2015, the company has floated around 14,000 distribution points. During these times, the company struggled to achieve meaningful growth.

The key to meaningful future growth will not be through pricing, but volume.

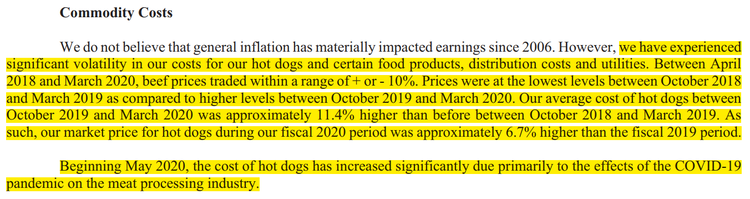

This is because the company lacks strong pricing power. Of the last 5 years, the company experienced 3 years of a decline in price. The fluctuation in price is a result of their pricing strategy, which is correlated to the cost of beef.

In the past few years, the cost of beef has fluctuated as much as 11% year-over-year. It is only expected to worsen during COVID-19.

The company believes there is still a large market for Branded Products, within existing accounts and larger accounts, because they believe the value proposition of a branded hotdog is extremely strong.

Nathan’s Branded Products appeals to other restaurants / venues because they do not want to sell just any hotdog. Most vendors want to serve something special while customers are watching baseball games, football games, movies in the theater, etc.. In order to differentiate themselves, they can partner with companies like Nathan’s to deliver something unique.

These captive markets are known for charging high prices. Imagine if you bought a hotdog at Yankees Stadium, only to find out that the hotdog stand not only charged you a fat price, but sold you a Bar-S hotdog, the cheapest one in the market and the most common one in the grocery store. Most customers would be infuriated.

Some vendors are willing to pay a higher cost to sell Nathan’s hotdogs. Others aren’t. It really just depends on the brand’s power in each geographic market where these venues are located.

The power of the Branded Products Program is only as strong as the brand associated with it.

Future of Restaurant Operations

The future prospects of Restauration Operations are attractive ONLY IF the company can pull off the restaurant transformation, especially with its franchises.

The operating margins for Restaurant Operations was once more than 20%. In the last 5 years, systemwide sales (company and franchised-owned) have decayed at a compounded rate of 4%. Since the decline, Restaurant Operations profits have decreased to less than 10%.

Many investors would be quick to dismiss the Restaurant Operations since it only represents 5% of profits today. However, if the company can rebuild the franchise system, Restaurant Operations could get back to 20% operating margins (which are even higher than Branded Products), it could deliver strong total free cash flow growth.

Nathan’s Famous faces many headwinds for its upcoming restaurant transformation, especially in the areas of branding and real estate.

My favorite book on branding is Brands and BullS**t. It was written by Bernard Schroder, my boss in college. He is a branding expert and worked with Jeff Bezos on Amazon in the early years.

He once told me, “brand repositioning is one of the hardest things for a company to do, if not the hardest.” Branding repositioning is essentially asking your customers to think differently about your company and interact with your company in a different way.

The transformation at Nathan’s Famous is no exception.

Founder Nathan Handwerker built the company on “serving a quality product for good value.” In the original Coney Island location, the company offered hotdogs for 5 cents, ½ the price of what its competitors were charging. They were always offering competitive prices. Nathan’s customers are used to relatively inexpensive food.

The company also built their brand on the pillar of convenience. Nathan’s is famous for their hotdogs. When you think of a hotdog, you think: quick, convenient, and cheap. Today, the company has found its home in “captive” markets like airports, stadiums, and movie theaters. Nathan’s found a great fit with these markets because they could serve their customers who were on the go. Like other hotdog or fast food companies, Nathan’s was never meant to be a destination restaurant.

The first challenge starts with brand repositioning.

The new menu features chef-created burgers, sandwiches, and side dishes. To spark your hunger and imagination, here’s a glimpse of some of the new items.

These new items are not the type of food that you can eat on the go. They’re also not the cheapest — every new item goes for $8.49.

Based on my estimates, the new menu is expected to generate an average ticket size of $8-14. The estimated average ticket size for the original menu was closer to $5-8. This is a 75% increase. The average restaurant would be happy with a 1-2% average ticket size increase.

As you can see, it would be very hard to make the case that Nathan’s (with its new menu) is a brand known for its “inexpensive” and “convenient” food.

There are three major implications to this.

Costs of turning away current customers — While some current customers may choose to put Nathan’s in their rotation of fast casual companies, other customers may be put off by the new menu and go somewhere else to fulfill their fast food needs.

Costs to acquire new customers — Nathan’s has not positioned themselves as a fast casual restaurant in the past. In order to inform customers about their new menu, they may have to spend more marketing dollars than their national advertising program allows (or that franchisees are capable of spending).

Competing in the “better burger” segment — James Walker stated that the move upstream was because he realized “we would never be in a position to compete with Subway, McDonald’s, Burger King on price.” Instead, he chose to compete in the equally competitive and equally saturated “better burger” segment where companies like Shake Shack reside. Since the rise of Shake Shack, there have been dozens of companies that have copied their model. Compare Shake Shack’s colors / design to the new restaurant model at Nathan’s. They are very, very similar.

The other challenge deals with location and real estate.

The customer visit is completely different with the new menu. To eat chef-cultivated food like this, you need more space to offer seating (as shown in the picture of new Nathan’s restaurant building).

Most of the current franchises are located in captive markets with small formats. To be a destination restaurant that offers seating and successfully executes a large, chef-inspired menu, Nathan’s will need to convince current franchisees or new franchisees to open a 3,000 square foot building and absorb all the related costs.

For current franchisees, they will most likely need to abandon their current location and select a new location. The location of Nathan's Famous, Wienerschnitzel, and Jack In The Box is very different from the location of Shake Shack, In-N-Out, and Chick-Fil-A. These locations are typically much more expensive as well.

Will Nathan’s Famous always have infinite ROIC?

I’ve found that questions around infinite returns on incremental invested capital are less about the actual business model and more about Management’s capital allocation philosophy.

Nathan’s business model focuses on leveraging an intangible asset, a brand, to generate growth in high margin businesses. There are certainly ways for competition to eat away at the company’s market share in licensing, branded products, or restaurants. And with a large enough decline in revenues, and subsequently profits, the business would certainly not generate infinite returns on capital.

However, that is more of a question about durability and longevity. For any business, returns would most certainly decline if the business is shrinking.

The question about future returns on invested capital is really about Management’s vision for the company. What kind of company does Management want Nathan’s to be?

The most troubling answer would be “a capital-intensive restaurant.”

Restaurant Capex Requirements

Compared to the total revenue of the business, the capital expenditures related to company-owned restaurants are very small.

Here’s the breakdown of the capital expenditures over the last 15 years.

The largest investments, both in percentage of revenue and dollar amount, occurred in 2010 and 2014. In 2010, Management spent $2.8M to relocate their office. In 2014, Management spent $4.3M to rebuild the Flagship Coney Island and Yonkers restaurants due to the devastation of Superstorm Sandy.

The investments in the other years can be viewed as maintenance capital expenditures because the spread between capital expenditures and depreciation is essentially 0%. Investments in the company-owned stores are necessary for the maintenance and cultivation of the Nathan’s Famous brand, especially at the flagship Coney Island location.

In the years without the one-time relocations, capital expenditures as a percentage of revenue averaged out to 2%. Because this percentage is relatively small, the only way for Management to dilute the infinite returns on invested capital is by making bad acquisitions of restaurants or overspending on company-owned restaurant expansion.

History of Poor Acquisitions

Nathan’s Famous has indeed made bad acquisitions in the past. When Nathan’s first went public in 1968, the company acquired Weston’s restaurant chain. Weston’s was a poor performing chain. Management believed they could take the struggling concept of Weston’s and combine it with the struggling concept of Nathan’s to form a stronger restaurant concept.

Wayne Norbitz was acquired as part of the Weston transaction. For the next two decades, the bad acquisition severely hurt the company and crippled it with debt. Then in the late 1990’s, the company acquired Kenny Rogers Roasters and Miami Subs, both poor-performing restaurant concepts. At the time, Howard Lorber was CEO and Wayne Norbitz was COO.

Again, the company believed they could take three struggling concepts and form a stronger one — this time by leveraging the co-branding. Wayne Norbitz should have known better, especially since he experienced the repercussions of the Weston acquisition first-hand. Both turned out to achieve subpar results and they eventually sold them less than 10 years later.

Today, Howard Lorber and Wayne Norbitz sit on the Board. Nathan’s Restaurant Operations are still struggling, as indicated by the decline in unit count, AUV, and systemwide sales. Additionally, the company has $77M in cash, 70% of which can be considered excess cash. The company has room to increase its debt load as well.

With a Management team that has made the same mistake in a row and a significant pool of dry powder, the company might feel obliged to “put the capital to work” by buying another restaurant concept, especially in an environment like this. Johnny Rockets was just sold to FAT Brands, and many other restaurants are expected to go on sale during the remainder of the pandemic.

Personal Incentives

In the company’s compensation structure, Management’s first three objectives relate to Restaurant Operations, even though 95% of the profit is generated through Licensing and Branded Products Program.

These incentives are important because most of their compensation comes from it. For the CEO and CFO, they receive 50%+ of their compensation from the company’s cash incentive plan.

Note that total compensation was temporarily reduced for both executives as a response to COVID-19.

It’s also important to consider James Walker, the Senior Vice President of Restaurants spearheading Restaurant Operations, when thinking about capital allocation. In a podcast with Restaurant Executive Mastery, James Walker described the plan for the new restaurant model this way (paraphrased): “the only way we can get franchises to get on board with the new model is if we do it ourselves in the company-owned stores.”

If James does what he says he does, there will most certainly be more investments into the company-owned restaurants. As illustrated below, the cost to uproot the old format to new format may be extremely expensive.

Last, but not least, the Board might not have an incentive to care. Director compensation at Nathan’s is really low, even at a small company like this. These Directors have been with the company for 15-35 years and may have been passive on poor capital allocation issues in the past.

Return of Capital to Shareholders

Historically, the company has paid out more than 100% of its free cash flow annually through a combination of buybacks, special dividends, and quarterly dividends.

So while Management may have every reason to over-invest in its restaurants or make bad acquisitions, it seems as if the high priority of returning capital to shareholders may prevent Management from making poor decisions that dilute the infinite returns on invested capital.

Key Questions

In this report, we’ve outlined how to think about Nathan’s Famous as if you were a long-term investor looking to buy the entire business. We’ve walked through everything you’d need to consider as a private business owner.

The essential information was provided to you in this report. Now it’s time for you to take your stance. Where do you fall on the issues of longevity, profitability, growth, and capital allocation?

Here are three pieces of advice as you continue to dig more into Nathan’s Famous:

Eat a Nathan’s Famous hotdog — Does it taste special, or does it taste like another hotdog?

Walk into your grocery store — How do these customers decide which hotdog to buy?

Talk to franchises — Do you think they are ready, willing, and able to adapt to the new restaurant model?

Thank you for reading. I hope to sharpen my skills every month and develop meaningful relationships along the way. What points do you agree with? What points would you like to share your own perspective?