2022 Annual Letter

2022 Annual Letter

Annual letter | 30 min read | Reflections on my third year of investing and my relationship with time

Third Annual Letter

To my friends on this value investing journey,

It is my pleasure to present to you my third Annual Letter. As I mentioned in prior letters, the theme of all letters will be summarized by this quote:

“We enjoy the process far more than the proceeds.” Warren Buffett

Aswath Damodaran makes a similar point when he says that valuation is not an art, nor it is a science; rather, it is a craft. And like all crafts, you learn by doing. The more you do it, the better you get at it.

In these letters, I will document my journey as a business owner — the good, the bad, and the ugly. I hope by writing these letters, you will find some things that you can take away to improve your own craft as an investor.

Reflecting on Three Years

I am very much in the early innings in my journey. This is my third year in the game. And I know I will be at this for a very long time.

These are formative years, the roots of my foundation, so I thought it would be good to summarize my development thus far.

—

Analyzing Businesses | 2019 - 2020

I started exploring the world of value investing in the summer of 2019. I made my first investment decision in 2020. I also spent five months publishing the Diligence Report series. This exercise taught me how to break down a business in its most essential components: durability, moat, quality, and capital allocation.

Looking back on those five write-ups, I could see that my analysis was good. I felt like I understood business just as well as anyone else. I knew that I had the potential to be a great business analyst. My prior experiences in consulting and venture capital were early confirmations of that.

But my game was far from complete. Value investing is much more than just understanding the quality of a business — it’s knowing how much to pay for that quality. It’s about decision-making. It’s learning how to frame an opportunity and knowing when to pull the trigger. It’s knowing where you might have an edge and recognizing the signs when it’s obvious that you do.

I didn’t have any experience in that. It’s primarily why I missed an opportunity to own Collectors Universe in February 2020. I couldn’t put the pieces together in a reasonable timeframe. Note: You can read more on that in my 2020 Annual Letter.

—

Framing Opportunities | 2021

In the pursuit of not letting that happen again, I decided to start the Traveling Through Time series. This was a case study series dedicated to improving my decision-making. In 2021, I simulated four opportunities that existed between 2013-16. I also did deep dives on three different opportunities.

By then end of the year, I walked away with a tried-and-tested framework to evaluate an opportunity:

Is it safe?

Is it cheap?

Is it good?

I also picked up other supplementary decision-making techniques. Note: You can read more on that in my 2021 Annual Letter.

Thus began my transformation from a business analyst to a business owner — someone who was actively putting money to work on behalf of his family and other investment firms.

—

Moving Fast | 2022

That brings us to 2022. Despite my improvement in decision-making, I have been facing a harsh reality: I might not be fast enough.

I am facing every young investor’s problem: I was getting more capital than I could handle.

In 2019, I had just graduated from college, so my capital base was virtually nothing. For the past three years, my capital base has grown rapidly. Even looking forward, I expect my capital base to grow by at least 60% by the end of 2023 and between 20-40% per year for the next several years.

Take a rapidly growing capital base and combine it with embryonic skills and you’ll find an investor who needs to find a lot of ideas. Even for a concentrated investor like myself (20%+ positions), this can be a problem.

Note: I position holdings based on future expected capital flows. But this isn’t a discussion on portfolio management. I am just trying to illustrate that these circumstances force me to have multiple ideas so that (a) I am not “locked” into to a bad idea with a concentrated position (I have a 2-year holding minimum) (b) I know which companies to own next once the next tranche of capital comes (which always comes faster than I expect).

Tracking Time: Results and Lessons

Given this problem, I set out to do one thing: track my time. For the year of 2022, I tracked every single minute that I spent on investing. I wanted to know one question: Am I spending my time well?

By seeing where every minute is spent, I would have a better idea on how to allocate my time in the future: per day, per week, per month, and per idea.

—

Building the System

To track my time, I created a simple system:

I created a worksheet for each month

The activity name was in the first column

The days of the month were on the header row

I captured each minute spent on a particular activity using a stopwatch

I inputted time spent per activity per day into the month’s worksheet

Each activity belonged to one of four categories:

General: Journaling, publishing (Substack), emails, or misc. meetings

Idea-related: Scuttlebutt trips and investment meetings related to ideas

Holdco: Companies that I owned at the beginning of the year

Pipeline: Companies that I did not own at the beginning of the year

This rolled up into a “Summary” worksheet for the year

Activity name in the first column

Months on the header row

The illustrations above are my actual results for the 2022 calendar year (with activities redacted, of course).

—

My Time in 2022

The remainder of this section will be answering the question I posed earlier: Did I spend my time well in 2022?

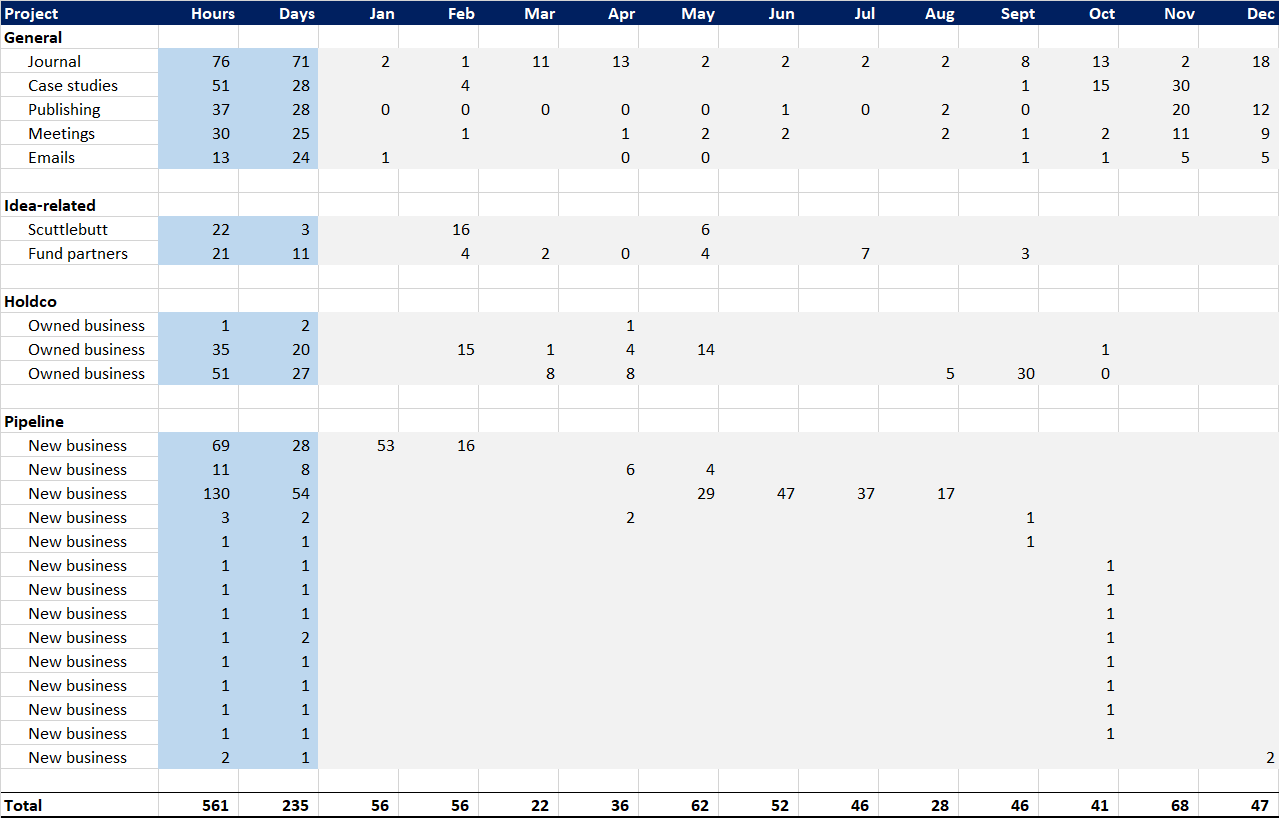

First, we have to look at my overall productivity. My overall hours spent puts into context what activities I did and how much time I spent on each one.

In the year of 2022, I was not a full-time investor. My full-time job is in Investor Relations. So, I spent mornings, evenings, and any spare minute that I had on investing.

My typical work routine started at 6:30 AM and ended at 6:30 PM. That gave me 12 hours of time for total work, at least 8 of which was spent on my full-time job and at most 4 hours on investing.

Therefore, 2.33 hrs sounded like a reasonable number of hours I could spend on investing each day — an hour in the morning, an hour in the evening, and some time in between.

I nearly achieved that goal. Here are the high-level results:

Days: I spent 235 days on investing. There were 313 workdays in the year (includes all holidays, excludes all Sundays). Therefore, I worked 75% of the 313 possible days of the year.

Hours: I spent 561 hours on investing. There were 730 work hours in the year (313 potential workdays x 2.33 hrs per workday). Therefore, I worked 76% of the potential 730 hours in the year. On average, I worked 2.4 hours per days.

For the most part, I consistently put in the work, day-in and day-out. I could have hit 85% of possible hours if I missed less days.

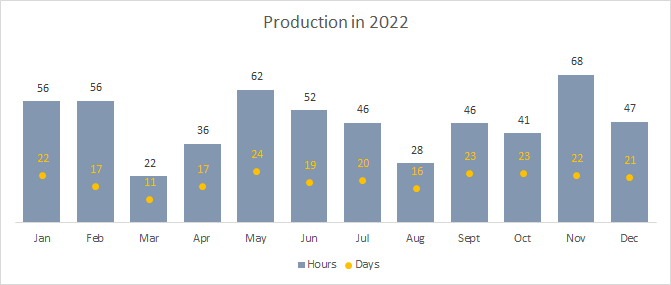

As you see in the chart, I had low levels of activity in the months of Mar, Apr, and Aug. During these months, I worked an average of 15 days as opposed to my normal clip of 20+ days.

Like most people, things pulled me away from work from time to time. So, I think my 76% production rate (of total hours) this year was quite good. I don't realistically see myself hitting 90%+. I think 80-90% is a realistic goal to target.

Now here's where the numbers start to get interesting. The following is a breakdown of my time spent across a few different categories.

General: I spent 206 hours, or 37% of my time, on general activities. Included in the general activities are journaling, publishing, emails, case studies, and misc. meetings.

Research: I spent 354 hours, or 63% of my time, on research activities. Included in this category are:

Idea-related: I spent 43 hours, or 8% of my time, on idea-related activities. Included in idea-related activities are scuttlebutt and talking with certain investment partners.

Holdco: I spent 87 hours, or 15% of my time, researching companies I owned at the beginning of the year.

Pipeline: I spent 225 hours, or 40% of my time, researching new opportunities.

Two questions arise.

Did I spend the right amount of time on the right categories?

Did I spend the right amount of time on each activity within each category?

—

Return on Invested Time on Non-Research Activities

It’s clear that I spent a good chunk of time, almost 40%, on non-research activities.

Ideally, that number should be a lot less. Because at the end of the day, researching ideas is what drives your returns... right?

From Jan to Sept, I was extremely focused on researching ideas. I spent 85%+ of my time on research activities.

During that nine-month period, I didn’t talk to any investors at all. My intake of overall content (blogs, podcasts) was quite low. I also didn’t focus on any case studies. Between my full-time job and other life activities, I was limited on time. I thought this level of focus would make me a stellar investor.

I mean, aren’t I passing Charlie Munger’s test: an investor that cannot be alone with their own thoughts for a long time are terrible candidates to become successful investors?

… And passing Buffett’s test: I just sit in my office and read all day?

In an attempt to move faster (the problem acknowledged at the beginning of this letter), I had possibly created another problem: Maybe I wasn’t getting better.

During that time, I felt like a man with a hammer who saw everything as a nail. I was getting through ideas, but I didn’t feel like I was improving my skills.

Maybe arrogantly, I believed that I had progressed to a level where I could rely on my own sense of style and decision-making motor. I didn’t need to challenge my beliefs, philosophies, or techniques as much as I had in the past.

Frederik Gieschen from Neckar’s Minds and Markets addresses part of this problem in his article, The Reading Obsession.

Did a young Buffett read a lot? Yes, he certainly did. Did he spend all his time churning through annual reports, newspapers, books, and trade journals enough? No. Buffett understood how to balance his stack of reading materials with a solid travel schedule. He did not expect to solve the world’s investment puzzles solely from the comfort of his desk.

He built and maintained relationships that allowed him to source and discard ideas and evolve as an investor (not to mention enrich his life). Just think about the influence that Munger had on his pivot towards quality investing.

…

“Buffett’s huge network of knowledgeable and influential friends also has been a help along the way. Buffett has been an original thinker, but it cannot have hurt to discuss prospects for a television station with Tom Murphy, chat about a common investment with Laurence Tisch, or talk with Jack Byrne about insurance. ‘His network of mends has been very important,’ says broker Hayes.” Of Permanent Value, The Story of Warren Buffett

…

Since childhood, he had read every biography he could find of people he admired, looking for the lessons he could learn from their lives. He attached himself to everyone who could help him and coattailed anyone he could find who was smart.

Frederick Gieschen makes it clear that young Buffett drew inspiration from and challenged himself with other investors.

In fact, the greatest investors, regardless of age or stage, seem to do this. When I met Tom Russo this year, he could not stop referencing Buffett, both his catechisms and his decisions.

So, during the last three months of the year, I shifted my approach. To make up for lost time, I spent virtually all of my time doing case studies, journaling about certain topics, and connecting with more investors than I ever had before.

Since I’m writing this in early January, there might be some recency bias to this, but I do feel like I became more of a well-rounded investor because of those last three months. More than ever, I feel like I can see both the forest and the trees.

So, the 40% of time spent on non-research activities — was that too much?

No, I don’t think that is a bad ratio in and of itself. It depends on the quality of those activities.

The case studies always generate very high returns and very quick paybacks. I pick up things that I can immediately use when analyzing the next opportunity. Case studies are one of the best things I can do, right next to research activities. I expect to do a lot more of them next year as well.

Journaling is a large bucket that includes a swath of different tasks: notetaking, reflecting, watchlists, executing trades, forecasting capital needs, strategizing portfolio, etc. There is a high chance these things are helpful, but the magnitude is harder to determine. Finding a way to do these things efficiently will be important going forward, especially because some of these tasks reach diminishing returns faster than others.

Connecting with investors (publishing/blogging, meetings, emails) can be hit-or-miss as well. The probability of something amazing coming out of it is quite low. But the reward, like a new investment idea or a job opportunity, can be very, very high. Finding a balance for this is tough, so one needs to approach it thoughtfully. Thankfully, I have seen many seeds blossom from connecting with investors this year.

So, I think targeting between 25-35% of my time on non-research activities will help me be a well-rounded investor while giving me enough time to do what matters: work on ideas.

—

Return on Incremental Invested Time on Research Activities

Here’s where it gets even more interesting.

There is the concept of return on investment. Then, there’s the concept of return on incremental investment. The latter is most important when looking at time spent on research activities.

When you’re looking at a new idea, the first hour provides incredible returns. Within an hour, you can immediately tell if this is something that should go on your watchlist. I would say 50% of my conviction in any stock comes from the first hour.

What might take place in this first hour? Looking at three things: the business description, the last 10-years of financials, and the price of the company.

After one hour, you have a way to frame the opportunity. You have a good sense of what could drive the investment results and what could hinder them. In this one hour, you can get 50% towards overall understanding or conviction in an idea.

Everything after that has diminishing returns.

After the first hour, you’re taking your frame (your hypothesis) and chasing down evidence to prove or disprove your hypothesis in a piece-meal way. I have yet to find a silver bullet — a source that gives everything you need to know within one hour.

Even the 10-K, which has the potential to provide significant benefits, never yields as much as 50% in return on invested time. Because of the way lawyers and accountants write filings, you’ll never get all the information you need. You might get clues, but never full answers.

I have always felt like investing is like playing a game of Clue, making guesses as to which sources of information can confirm the most important aspects of the thesis. I have found this to be especially true in microcap land where information isn’t readily available. You have to piece together research yourself.

With this concept of incremental invested returns in mind, I want to take a deeper dive into the opportunities I researched.

—

Looking Into New Ideas

Remember, my goal for the year was to work faster and hopefully work through more ideas.

In total, I looked at 14 new companies.

For 12 of those, it was only an initial pass. On average, I spent one hour on each idea. Those 12 hours provided very good returns. Within that short amount of time, I was able to build a watchlist and rank the ideas that could have the highest, but safest forward rate of return.

For the remaining two companies, I spent 70 hours and 140 hours researching each one, respectively.

For the first company, 70 hours was not the total amount of time spent on the project. It was about 150. I spent about 80 hours researching the company in 2021. The second company was completely new to me. The 140 hours encapsulates that entire research process.

For both companies, I was considering making them 20% positions and holding them for a minimum of 2 years. I ended up not buying either of them. They currently sit on my watchlist.

One question arises from here: was that time spent well?

Most people would say that time was wasted. No one would ever spend 150 hours on a stock they wouldn’t own. Of course, if I bought the companies, people would say otherwise.

I think it’s less black and white than that. Instead of comparing the time to the result, I believe it’s more useful to evaluate the overall process. These two questions stand out in my mind:

Was there a point at which I knew I didn’t want to buy it, but forced myself to finish anyways?

Did I prioritize activities within my research process poorly?

There could be a much, much longer discussion exploring these two questions for those two companies. At a high-level, I have come to admit that I did not spend my time as effectively as I should have with:

… the first company because, at some point, I knew I didn’t want to buy it and I did not prioritize tackling the investment issues that drove my uncertainty.

… the second company because I did not prioritize tackling certain issues first.

In conclusion, I spent the right amount of time looking at new ideas, but I could have reallocated some of the time between the different ideas — ideas that were more actionable, more within my circle of competence, or simply bets with better forward returns.

So, how do I structure my research process so that I don’t run into these problems in the future?

Becoming The Fastest Draw in the West

To move faster and with more precision, I am going to draw out some techniques/frameworks from my favorite book of 2022, How to Write Fast (While Writing Well). It’s the same book I referenced in my most recent article, Investing Is My Art, Writing Is My Tool.

There are two lines from the book that capture the essence of this annual letter:

“I can write faster than anyone who can write better and better than anyone who can write faster.”

“Writing can be joyful and liberating and fast.”

Let me convert that into an investing context: I want to be an investor who can make decisions better than anyone who’s faster, and faster than anybody who’s better.

My ambition is after the reputation that Warren Buffett had built by 1966:

“So Charlie goes back in the room with me. And after about half an hour, Ben [Rosner] was jumping up and down, and he said, ‘They told me you were the fastest gun in the West! Draw!’ And I said, ‘I’ll draw on you before I leave this afternoon.’”

Warren Buffett, quoted in The Snowball (Chapter 29: What a Worsted Is)

I also want investing to feel joyful and liberating and fast. This is also similar to what Warren Buffett said toward the end of his partnership years:

“I would like to have an economic goal which allows for considerable noneconomic activity... I am likely to limit myself to things which are reasonably easy, safe, profitable, and pleasant.”

David Fryxell’s How to Write Fast (While Writing Well) contains ideas that I believe, if truly internalized, can help me, at the very least, become a better and faster investor, and, at the very most, an investor who feels like the craft is joyful and liberating and fast.

—

#1 Optimize Creative Pressure

To work through more ideas, I can simply spend more time on investing. Every minute counts. Making the most of spare moments — that’s the easiest way to increase output.

In his book, David Fryxell recounts a story in which a writer finished writing a novel in one year simply using the 10 mins his wife routinely late to dinner. That’s the power of those spare moments.

However, it’s not just about taking advantage of spare moments — that can only get you so far. It’s about organizing your entire work schedule to have more flow and precision. David Fryxell says the best way to do this is by building “creative pressure.”

The technique of creative pressure is based on the principle of closure. Our minds naturally seek closure. If you were to draw a circle that was only 3/4 finished, your brain can actually trick your eyes into thinking it is a full circle. The subconscious is a powerful weapon in your arsenal and should be used as much as possible.

This is the spirit of Ernest Heminway’s writing rule: “stop while you're going good.”

Hemmingway’s rule was to end a writing session by taking some baby steps into tomorrow’s territory. Instead of closing up shop when today's section — or whatever — was finished, Hemmingway started on the next paragraph as well. And then, after a few lines, he’d abruptly stop, in the middle of a sentence…

... Why? Because, this way, he guaranteed himself an easy start the next day. After all, he had already figured out how to continue the story. The words were already — or: still — there, stored in his unconscious mind.

This technique can be applied to investing. For example, scheduling deep research in the morning as well as in the evening creates a natural conduit for flow and creative pressure, allowing both the conscious and subconscious to tackle difficult questions when researching an opportunity.

—

#2 Find Fast Ideas

To work through more ideas, I have to realize that ideas are cheap, but time is not.

What does that mean?

There are a lot of investment ideas out there. Every idea hinges on two factors:

What is important?

What is knowable?

Even if it checks off both boxes, not every investment idea is a worthwhile endeavor. Just because I have the ability to research the knowable and important factors doesn’t mean that it is a valuable idea. David Fryxell recommends that you should only write the stories that you can write. The same suggestion certainly applies to investors.

Finding fast ideas takes deep humility of your current knowledge and abilities, your current schedule, and your other opportunities costs. That’s why finding your style is critical to the investment process. I’ll be writing much more on this topic in 2023.

—

#3 Know Where You Are Going

And lastly, working through ideas with more speed and precision requires that you know where you are going.

This may seem obvious, but it has been a consistent hurdle for me in these early years. As a buy-and-hold investor with a minimum 2-year holding period, I have tended to get lost in the trees and forget about the forest. I also genuinely like learning about businesses and can spend many hours in a room simply reading and thinking without any action.

David Fryxell uses the term “generalship” to encourage writers to develop a research strategy that captures all the facts you need and covers as little extraneous territory as possible. In other words, being a lazy researcher and a precise writer.

As an investor, this gave me a new appreciation for the importance of framing and handicapping.

It’s critical, from the beginning, to think about which factors need to be in play for an investment idea to work, to estimate how long it would take (based on the known/available sources) to research those factors, and to identify which areas could be a black hole of time.

This year, I have incorporated new systems into my process that I hope will aid my generalship efforts. Some of these include preliminary blueprints, critical maps, among others.

One particular technique I am excited to use is a “time trigger.” It’s essentially forcing myself to stop at certain time intervals so that I can consider continuing or exiting. Right now, I have set time triggers at the 1-hour, 5-hour, 10-hour, 20-hour, 35-hour, and 50-hour mark. These give me exit ramps to move onto other ideas and possibly revisit it at another time.

—

My hope is that these ideas so fundamentally shift the way I view the research process to the point where I develop habits and systems that give me the speed, momentum, and precision to work through more ideas.

Liberated by Eternity

The Burdens of Production

There’s a lot of pressure that comes with trying to move fast, be more precise, and be more productive.

Every minute counts, and that realization is a heavy burden. Spare moments not spent on investing are wasted opportunities. Spending time on the wrong things also feels painful. Even spending time on the right things, but the wrong amount of time on them, really hurts.

At some point, time suddenly became an investment even more important than money. It was hard not to be in conversations with friends without thinking, “I could be reading something right now.” Even doing good deeds like helping friends move or picking up medicine became bitter tastes in my mouth. Everything was an investment, and I was missing out every single second.

My goals of maximizing efficiency and effectiveness turned into chains of unhappiness and unrest.

At one point, I did not really enjoy the craft of investing — a scary thought for a part-time investor who had aspirations of making this “full-time” at some point. I even had an idea of creating a ground-breaking investment partnership. I wanted investing to feel joyful, liberating, and fast, but I often felt frustrated, discouraged, and slow.

—

Leaf by Niggle

I wasn’t too unlike J.R.R Tolkien when he was working on The Lord of the Rings.

Note: The following quotes are excerpted from Tim Keller’s book, Every Good Endeavor.

When J.R.R. Tolkien had been working on writing The Lord of the Rings for some time, he came to an impasse. He had a vision of a tale of a sort that the world had never seen.

…

He began to despair of ever completing the work of his life. It was not just a labor of a few years at that point. When he began The Lord of the Rings, he had already been working on the languages, histories, and stories behind the story for decades. The thought of not finishing it was "a dreadful and numbing thought."

He feared he had run out of skill and luck. In attempt to put a voice to his internal struggle, Tolkien began writing a short story called Leaf by Niggle. In this story, an artist, named Niggle, lives in a society that does not value art.

The Oxford English Dictionary, to which Tolkien was a contributor, defines “niggle” as “to work… in a fiddling or ineffective way… to spend time unnecessarily on the petty details.”

…

Niggle had one picture in particular that he was trying to paint. He had gotten in his mind the picture of a leaf, and then that of a whole tree. And then in his imagination, behind the tree " country began to open out; and there were glimpses of a forest marching over the land, and of mountains tipped with snow." Niggle lost interest in all his other pictures, and in order to accommodate his vision, he laid out a canvas so large he needed a ladder.

…

[But] Niggle "had a long journey to make. He did not want to go, indeed the whole idea was distasteful to him; but he could not get out of it." Niggle continually put the journey off, but he knew it was inevitable. Tom Shippey, who also taught Old English literature at Oxford, explains that in Anglo-Saxon literature the "necessary long journey" was death.

….

Niggle knew he had to die, but he told himself, "At any rate, I shall get this one picture done, my real picture, before I have to go on that wretched journey.”

So he worked on his canvas, "putting in a touch here, and rubbing out a patch there," but he never got much done. There were two reasons for this. First, it was because he was the "sort of painter who can paint leaves better than trees. He used to spend a long time on a single leaf,.. " trying to get the shading and the sheen and the dewdrops on it just right. So no matter how hard he worked, very little actually showed up on the canvas itself. The second reason was his "kind heart." Niggle was constantly distracted by doing things his neighbors asked him to do for them. In particular, his neighbor Parish, who did not appreciate Niggle's painting at all, asked him to do many things for him.

…

While working desperately on his unfinished picture, the Driver comes to take Niggle on the journey he has put off. When he realizes he must go, he bursts into tears. Oh, dear!' said poor Niggle, beginning to weep, "And it's not even finished!?" Sometime after his death the people who acquired his house noticed that on his crumbling canvas his only “one beautiful leaf had remained intact.”

…

But the story does not end there. After death Niggle is put on a train toward the mountains of the heavenly afterlife. At one point on his trip he hears two Voices. One seems to be Justice, the severe voice, which says that Niggle wasted so much time and accomplished so little in life. But the other, gentler voice ("though it was not soft"), which seems to be Mercy, counters that Niggle has chosen to sacrifice for others, knowing what he was doing.

As a reward, when Niggle gets to the outskirts of the heavenly country, something catches his eye. He runs to it- and there it is:

"Before him stood the Tree, his Tree, finished; its leaves opening, its branches growing and bending in the wind that Niggle had so often felt or guessed, and yet had so often failed to catch. He gazed at the Tree, and slowly he lifted his arms and opened them wide. 'It is a gift!' he said."

The world before death his old country had forgotten Niggle almost completely, and there his work had ended unfinished and helpful to only a very few. But in his new country, the permanently real world, he finds that his tree, in full detail and finished, was not just a fancy of his that had died with him. No, it was indeed part of the True Reality that would live and be enjoyed forever.

—

The Invitation

Tim Keller, the author who reflects on J.R.R Tolkien’s story, makes an invitation to the J.R.R Tolkien’s and Niggle’s of the world — to liberated by eternity:

Once or twice in your life you may feel like you have finally “gotten a leaf out.”

Whatever your work, you need to know this: There really is a tree. Whatever you are seeking in your work—the city of justice and peace, the world of brilliance and beauty, the story, the order, the healing—it is there. There is a God, there is a future healed world that he will bring about, and your work is showing it (in part) to others. Your work will be only partially successful, on your best days, in bringing that world about. But inevitably the whole tree that you seek—the beauty, harmony, justice, comfort, joy, and community—will come to fruition. If you know all this, you won’t be despondent because you can get only a leaf or two out in this life. You will work with satisfaction and joy. You will not be puffed up by success or devastated by setbacks.

…

Artists and entrepreneurs can identify very readily with Niggle. They work from visions, often very big ones, of a world they can uniquely imagine. Few realize even a significant percentage of their vision, and even fewer claim to have come close. Those of us who tend to be overly perfectionistic and methodical, like Tolkien himself, can also identify strongly with the character of Niggle.

But really — everyone is Niggle. Everyone imagines accomplishing things, and everyone finds him- or herself largely incapable of producing them. Everyone wants to be successful rather than for-gotten, and everyone wants to make a difference in life. But that is beyond the control of any of us. If this life is all there is, then everything will eventually burn up in the death of the sun and no one will even be around to remember anything that has ever happened. Everyone will be forgotten, nothing we do will make any difference, and all good endeavors, even the best, will come to naught.

Unless there is God. If the God of the Bible exists, and there is a True Reality beneath and behind this one, and this life is not the only life, then every good endeavor, even the simplest ones, pursued in response to God's calling, can matter forever. That is what the Christian faith promises.

I initially read this story a few years ago. After a year of focusing on maximization, production, and speed, I re-read this story with a different lens. It hit home.

Today, I hold steadfast to the promise that eternity can TRULY make investing feel joyful, liberating, and fast. It changed my life. It could possibly change yours too.

Wherever you are in your journey, I encourage you to take some time to think about your relationship with time. I appreciate each and every one of you who has helped me on my journey as an investor and I look forward to our friendship for many more years to come.

Sincerely,

Ralph Molina

January 5, 2023

Great work Ralph!

You’ve definitely developed much as a writer over these few short years. Keep up the good work and self-reflection.